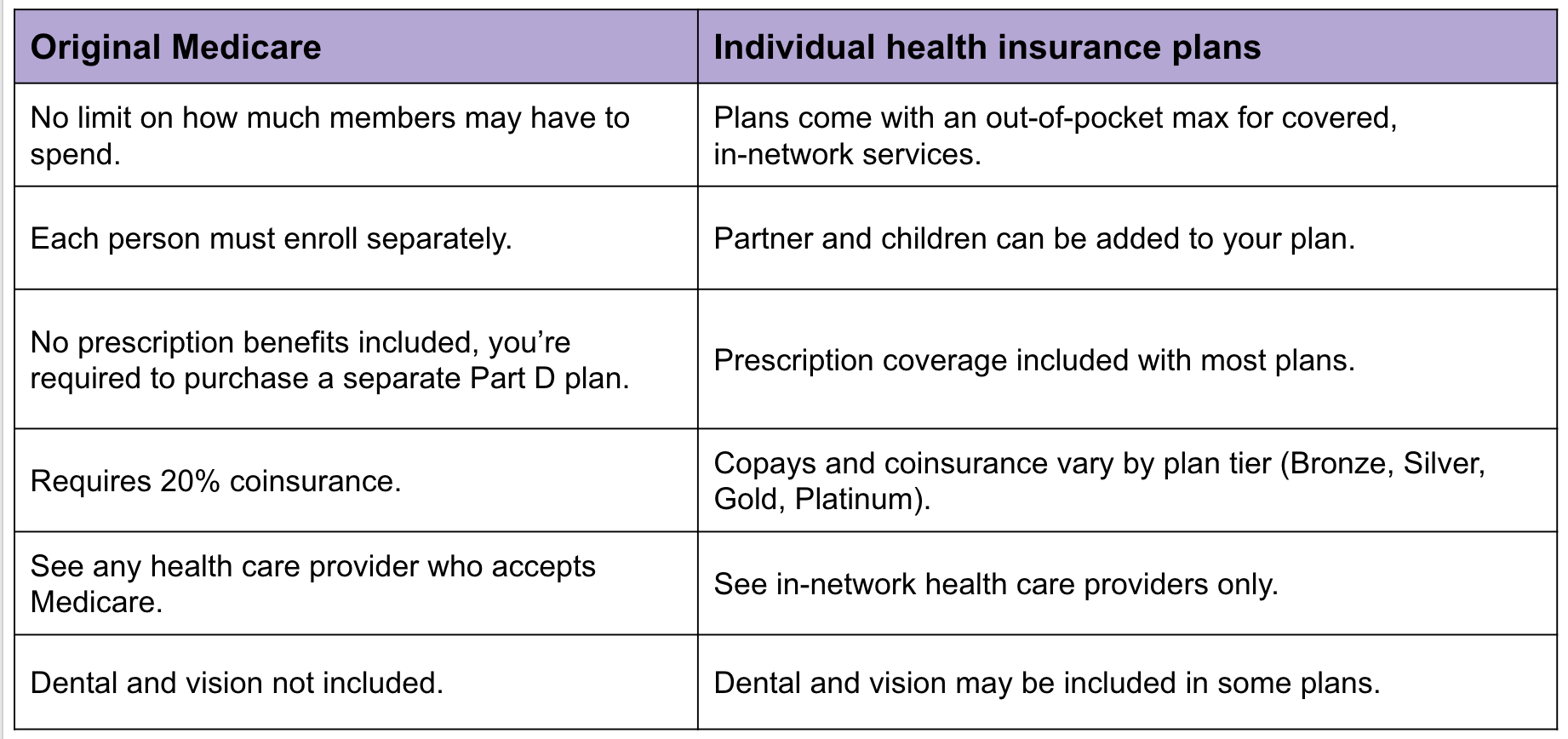

Some Of Paul B Insurance

Related Subjects One reason insurance policy problems can be so confounding is that the healthcare market is constantly transforming as well as the coverage intends used by insurance firms are difficult to categorize. Simply put, the lines between HMOs, PPOs, POSs and various other types of coverage are commonly blurred. Still, understanding the makeup of various strategy types will certainly be useful in reviewing your alternatives.

PPOs typically use a larger selection of carriers than HMOs. Premiums might be similar to or a little more than HMOs, and also out-of-pocket costs are normally higher as well as more challenging than those for HMOs. PPOs allow participants to venture out of the provider network at their discretion and also do not require a recommendation from a key care doctor.

As soon as the deductible amount is gotten to, additional health and wellness expenditures are covered in accordance with the arrangements of the medical insurance policy. A staff member might then be accountable for 10% of the expenses for treatment obtained from a PPO network copyright. Deposits made to an HSA are tax-free to the employer and worker, as well as cash not invested at the end of the year might be surrendered to spend for future medical expenses.

The Definitive Guide to Paul B Insurance

(Company payments must coincide for all workers.) Workers would certainly be responsible for the initial $5,000 in medical costs, however they would certainly each have $3,000 in their personal HSA to spend for medical costs (and also would have much more if they, as well, added to the HSA). If workers or their households tire their $3,000 HSA slice, they would certainly pay the following $2,000 expense, whereupon the insurance coverage would start to pay.

(Certain restrictions might relate to highly made up individuals.) An HRA must be funded exclusively by a company. There is no limit on the amount of cash a company can add to employee accounts, however, the accounts may not be moneyed through worker wage deferments under a cafeteria plan. Furthermore, employers are not allowed to reimburse any kind of component of the equilibrium to staff members.

Do you know when the most fantastic time of the year is? The magical time of year when you get to contrast wellness insurance policy prepares to see which one is best for you! Okay, you got us.

4 Easy Facts About Paul B Insurance Explained

Yet when it's time to select, it's important to recognize what each plan covers, just how much it sets you back, and where you can utilize it, right? This things can feel complicated, however it's much easier than it appears. We created some sensible discovering steps to aid you feel certain about your alternatives.

(See what we did there?) Emergency treatment is frequently the exemption to the guideline. These strategies are the most prominent for individuals who get their medical insurance via work, with 47% of covered employees registered in a PPO.2 Pro: A Lot Of PPOs have a decent choice of providers to select from in your location.

Con: Higher premiums make PPOs a lot more pricey than other sorts of plans like HMOs. A health and wellness upkeep organization is a health insurance strategy that normally just covers treatment from doctors who work for (or contract with) that certain strategy.3 So unless there's an emergency situation, your plan will not pay for out-of-network care.

The Single Strategy To Use For Paul B Insurance

Even More like Michael Phelps. The plans are tiered according to how much they set you back and also what they cover: Bronze, Silver, Gold as well as Platinum. (Okay, it's true: The Cre did have some platinum records and Michael Phelps never ever won a platinum medal at the Olympics.) Secret fact: If you're eligible for "cost-sharing decreases" under the Affordable Treatment Act, you need to select a Silver strategy or much better to get those reductions.4 It's excellent to recognize that plans in every category provide some kinds of complimentary precautionary care, and also some offer totally free or affordable medical care services prior to you satisfy your deductible.

Bronze strategies have the most affordable monthly premiums however the highest possible out-of-pocket expenses. As you function your means up through the Silver, Gold as well as Platinum groups, you pay much more in costs, yet less in deductibles and coinsurance. However as we mentioned before, the additional prices in the Silver category can be reduced if you certify for the cost-sharing reductions.

Reductions can reduce your out-of-pocket medical care sets you back a lot, so get with one of our Supported Neighborhood Companies (ELPs) that can aid you locate out what you may be eligible for. The table below shows the percentage that the insurer paysand what you payfor protected expenditures after you fulfill your insurance deductible in each strategy group.

Getting The Paul B Insurance To Work

Other costs, commonly called "out-of-pocket" prices, can build up quickly. Points like your insurance deductible, your copay, your coinsurance quantity as well as your out-of-pocket maximum can have a large effect on the overall cost. Below are some expenditures to keep close tabs on: Deductible the quantity you pay before your insurance provider pays anything (other than for complimentary preventative care) Copay a collection quantity you pay each time read more for things like medical professional brows through or various other services Coinsurance - the percentage of medical care services you are in charge of paying after you have actually hit your insurance deductible for the year Out-of-pocket maximum the yearly limitation of what you are in charge of paying on your very own you could try this out One of the most effective methods to save cash on medical insurance is to utilize a high-deductible health plan (HDHP), especially if you don't anticipate to consistently utilize clinical services.

When choosing your medical insurance strategy, don't ignore health care cost-sharing programs. These job virtually like the various other health insurance policy programs we described already, yet practically they're not a form of insurance coverage. Permit why not try here us to discuss. Health and wellness cost-sharing programs still have month-to-month premiums you pay as well as specified insurance coverage terms.

If you're attempting the DIY route as well as have any type of sticking around questions about medical insurance strategies, the specialists are the ones to ask. And also they'll do even more than just answer your questionsthey'll also find you the very best cost! Or perhaps you would certainly such as a method to integrate obtaining excellent medical care insurance coverage with the possibility to aid others in a time of demand.

The Greatest Guide To Paul B Insurance

CHM assists families share health care costs like clinical tests, maternal, hospitalization and surgical procedure. Plus, they're a Ramsey, Relied on partner, so you understand they'll cover the medical expenses they're supposed to and also honor your insurance coverage.

Secret Concern 2 Among the important things healthcare reform has actually carried out in the united state (under the Affordable Treatment Act) is to present even more standardization to insurance policy strategy advantages. Prior to such standardization, the benefits provided different dramatically from strategy to plan. For instance, some plans covered prescriptions, others did not.